|

Our review of procurement files and interviews with

Department staff found that:

§

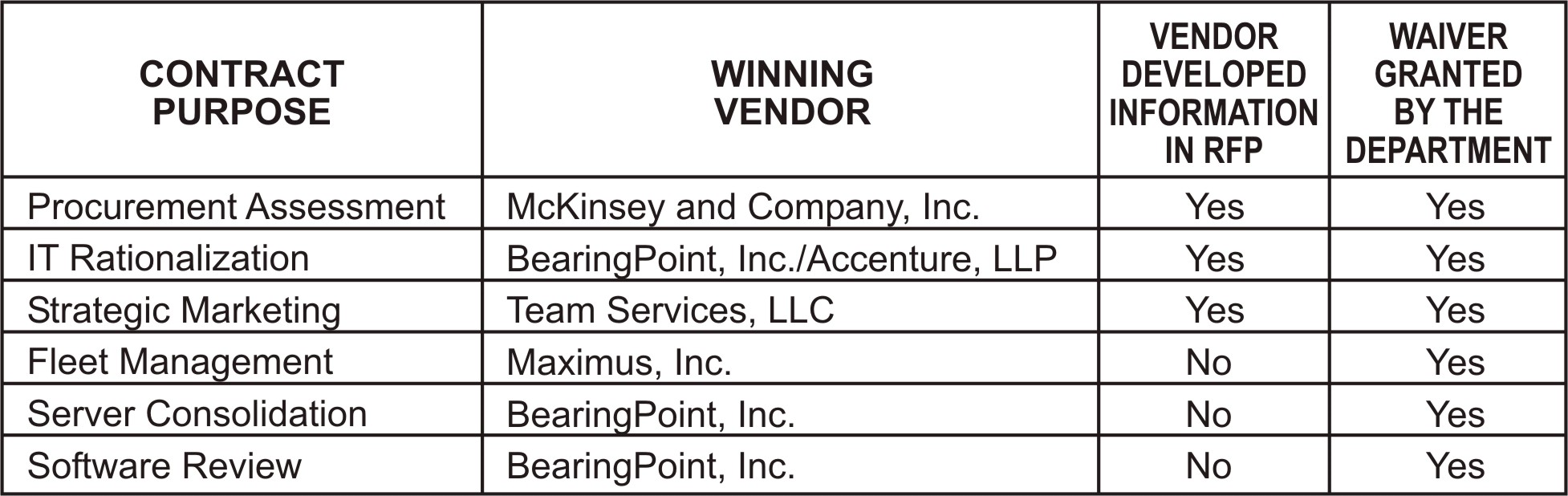

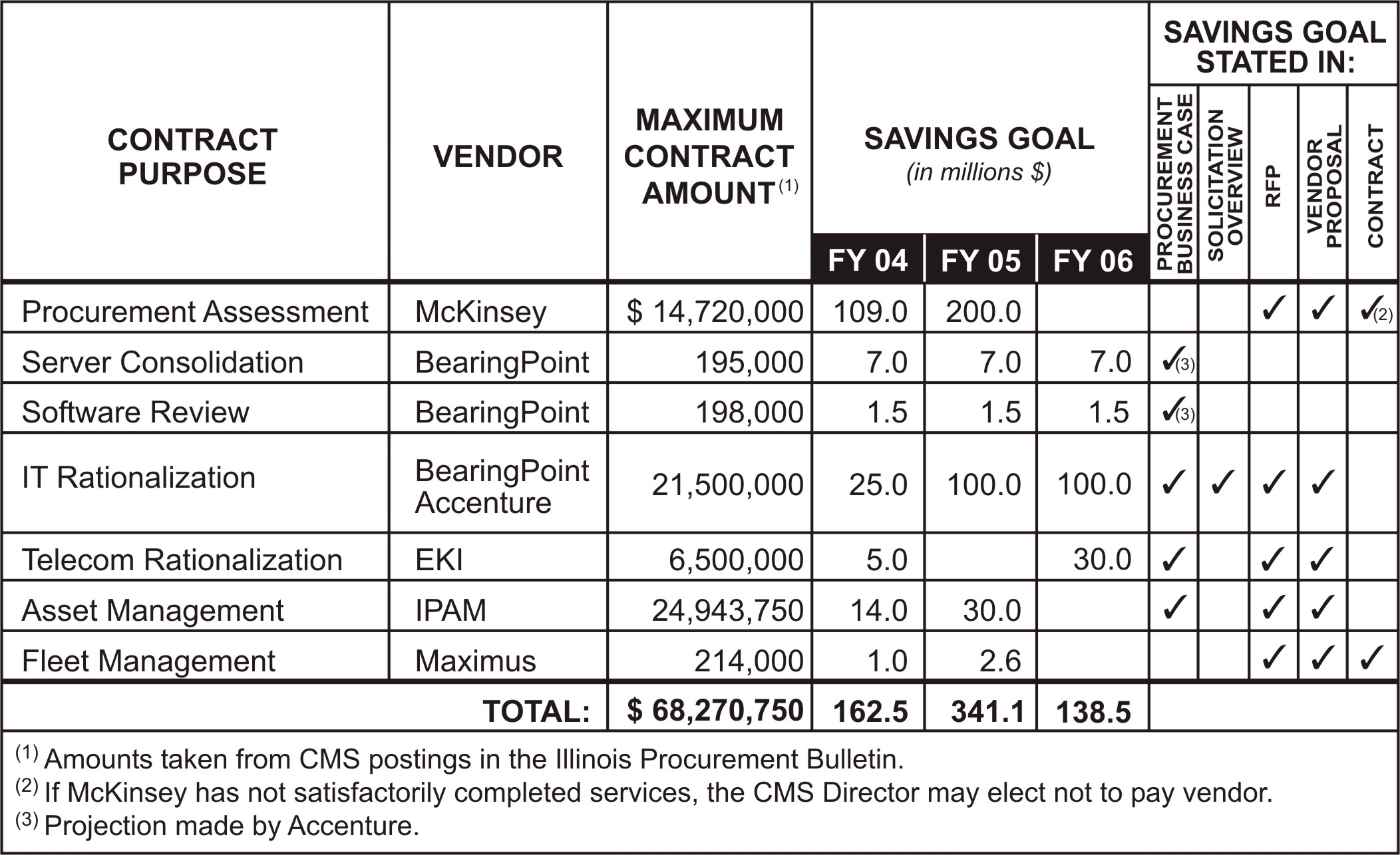

The Department utilized McKinsey and Company, Inc.

(McKinsey) to gather information on procurement spending by State

agencies. According to a Department

official, this work was performed on a pro bono basis for the State. McKinsey was listed as the source for much

of the factual information in the Procurement Assessment RFP.

§

The Department utilized Accenture to perform a

strategy study in the IT area.

Expenditure information in the IT Rationalization RFP was attributed

to Accenture, LLP.

§

The Department utilized Team Services, LLC (Team

Services), under a non-competitively bid contract, to provide contractual

assistance to the Department in an extremely similar project to what was

eventually awarded to Team Services as the Strategic Marketing

Initiative. The work performed on

this no-bid contract overlapped with the issuance of the RFP for the Strategic

Marketing Initiative.

The Department has adopted general guidelines that prohibit a

person who prepared the specifications from submitting a bid or proposal

unless the agency head determines in writing that accepting such a bid or

proposal would be in the State's best interest (44 Ill.Adm.Code 1.2050

(i). A notice to that effect must be

published in the Procurement Bulletin.

From our review of the procurement files for these contracts,

we could not find evidence the Department determined in writing that there

would be no substantial conflict of interest by allowing vendors to assist in

specification development and bid on the procurement opportunity and that it

was in the best interest of the State to accept bids from these vendors. Notices also were not posted in the

Procurement Bulletin – as required by the Illinois Administrative Code.

We also noted that the Department had a non-State employee

review the RFP for the Procurement Assessment prior to the release of the

RFP. This individual subsequently was

named as partnering with the winning vendor, McKinsey, in its proposal. (Finding Code No. 04-3, page 19)

We recommended that the Department review its process for

utilizing vendors to provide assistance in developing specifications and

information to be included in Requests for Proposals so as to not prejudice

the rights of other prospective bidders or offerors and the public.

The

Department disagreed with the auditor's findings.

CHANGES

IN AWARD EVALUATION CRITERIA NOT COMMUNICATED TO PROPOSERS

The Department evaluated vendor proposals using evaluation

criteria that was not stated in the Request for Proposals (RFP). Changes in scoring methodology were not

communicated to proposing vendors or reflected in an addendum to the RFPs. Additionally, in one of these instances,

the Department awarded a contract to a vendor that had not received the

highest scoring total based on evaluation criteria set out in the RFP.

The Illinois Administrative Code states that proposals shall

be evaluated only on the basis of evaluation factors set forth in the

RFP. (44 Ill. Adm. Code 1.2035

(h)(2)). However, we found in 44

percent (4 of 9) of the contracts we reviewed, the Department used different

criteria when evaluating the price component of the proposals. For instance, in the Risk Assessment,

Server Consolidation, and Software Review contracts, the RFP's identified a

single formula for evaluating pricing while, in practice, the Department used

two pricing categories - one for fixed price and another for a blended

rate. However, we noted that this

change in evaluation methodology - while not communicated to proposers - did

not appear to affect the contract award.

A similar problem was noted with the Fleet Management contract.

We recommended that the Department follow evaluation criteria

stated in Requests for Proposals when evaluating and awarding State

contracts. Additionally, the

Department should develop addendum to Request for Proposals when it

determines there needs to be a change to the evaluation criteria so that all

vendors are assured of a fair and open contracting process.

The Department disagreed with the finding.

EXTENSIVE VENDOR REVISIONS TO PROPOSAL

DURING BEST AND FINAL PROCESS

The Department allowed a vendor to extensively revise its

proposal during the best and final process after initial scoring evaluations

were completed. Several items deleted

by the vendor during the best and final process eventually were added back

into the agreement, in the form of contract amendments. The amendments, potentially costing the

State $5.75 million, were entered into after the award of the contract.

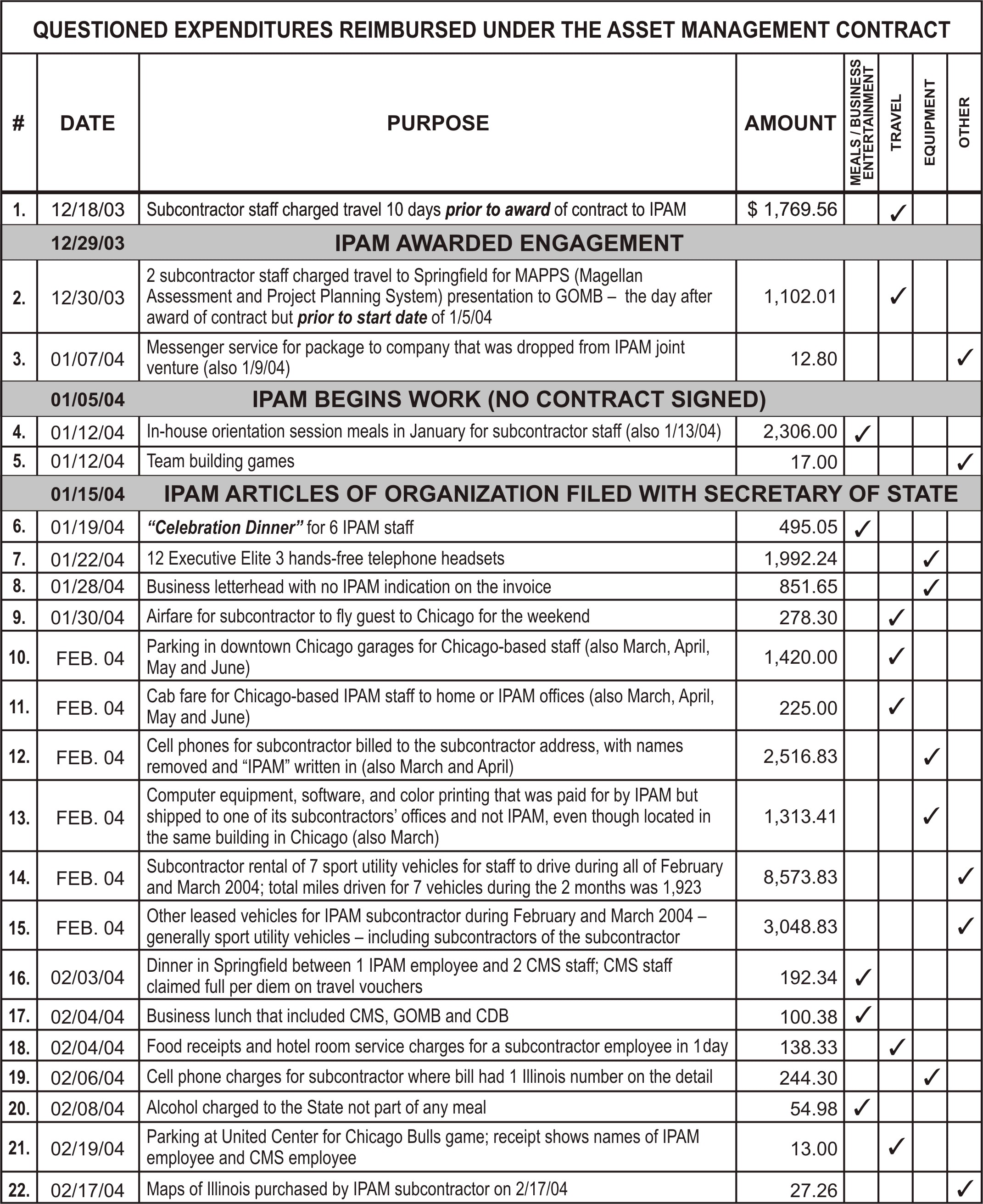

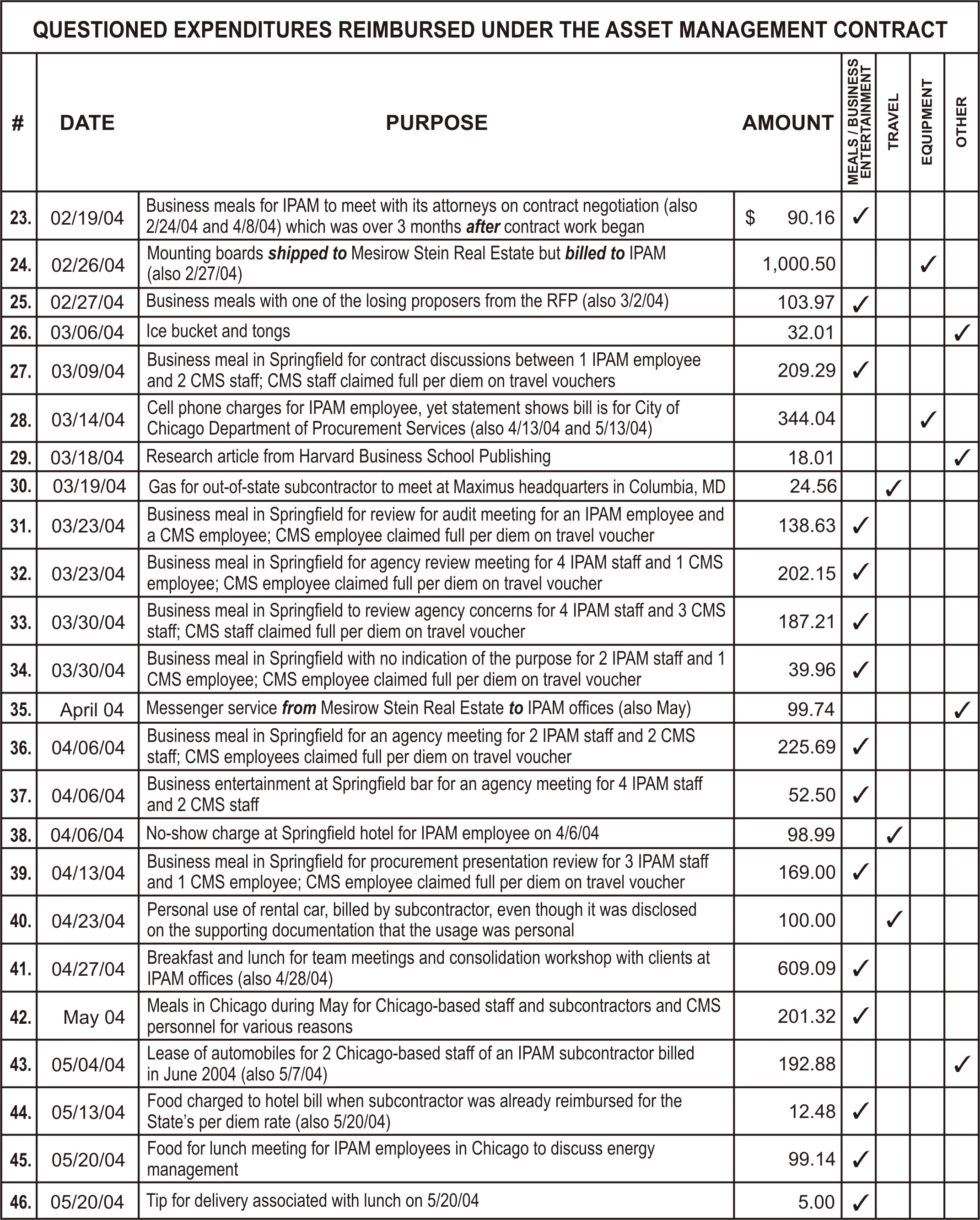

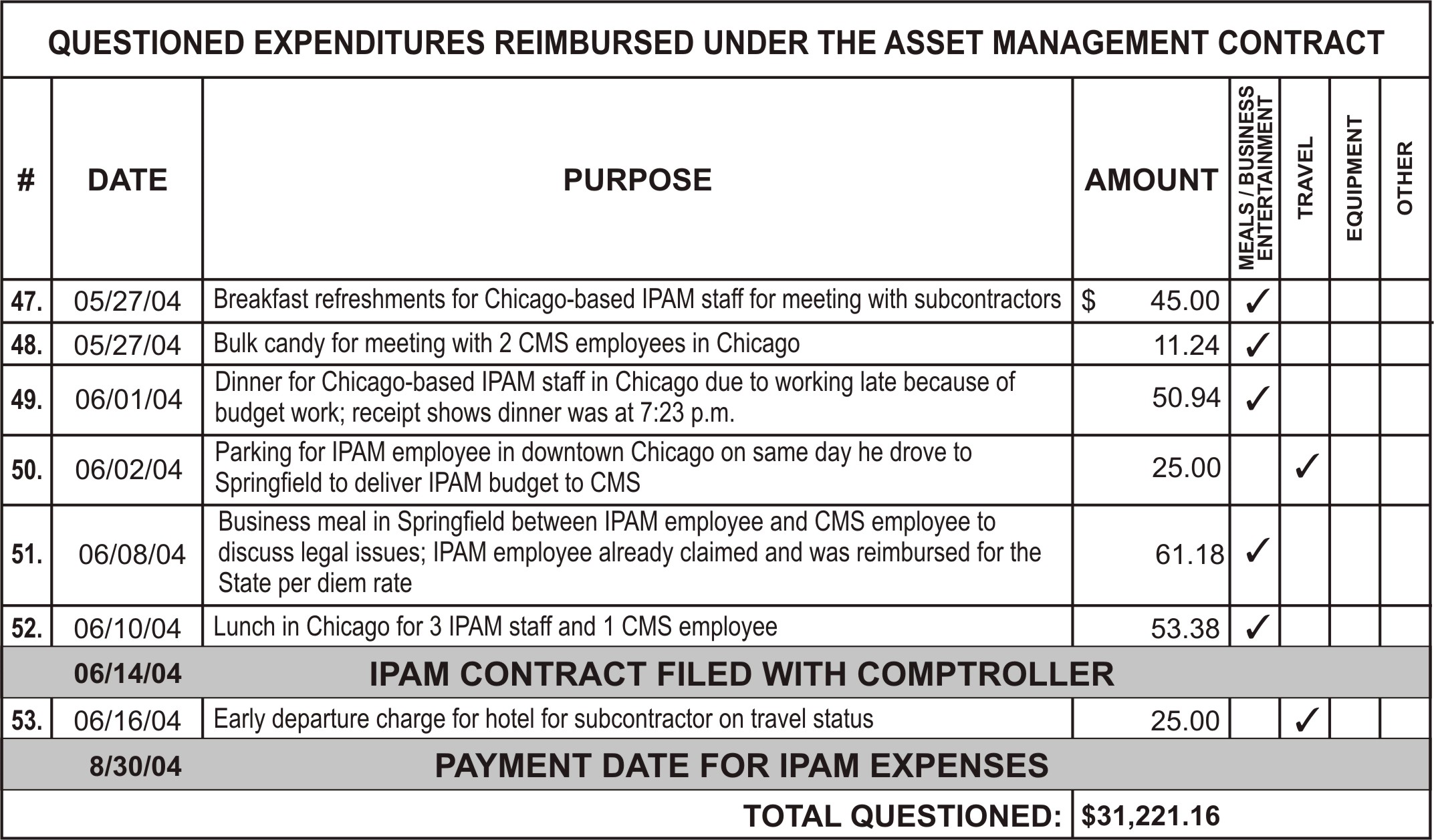

Documentation contained in the procurement files for the

Asset Management professional services procurement opportunity showed that only

one proposing vendor, Illinois Property Asset Management, LLC (IPAM), was

provided the opportunity to submit a best and final offer (BAFO). The Department’s correspondence to IPAM

states, “The purpose of this BAFO is to provide you with an opportunity to

enhance the pricing and to improve any of the services offered within your

original proposal.” While the price

decreased from $35.9 million to $24.9 million as a result of the best and

final process, IPAM’s technical proposal also significantly changed. Our review of the original proposal and

BAFO submitted by IPAM noted the following:

Revision of Joint Venture Composition: IPAM did not exist as an entity at the

time proposals were submitted, evaluations were conducted, or an award was

made. In its original proposal, IPAM

was to be a joint venture of two established firms, Mesirow Stein Development

Services and New Frontier Companies, and a “To be determined M/WBE

(minority/women’s business enterprise)” that would represent 20 percent of

the ownership. Background and

staffing qualifications were valued at 475 of 800 (59 percent) of the total

evaluation points. After the

initial proposals had been scored for background and staffing, IPAM dropped

New Frontier Companies as one of the joint venture partners. Further, according to Department staff, no

M/WBE firm had been named by IPAM as of December 14, 2004.

Revision of Performance Guarantee: The performance guarantee was valued at 50 of 800 (6

percent) total evaluation points. In

its BAFO, IPAM revised the performance guarantee from 5 items in the original

proposal down to 2 in the BAFO. A

Department official noted that IPAM did not hit its $14 million savings goal

in FY04 but that the IPAM fee was not adjusted downward because the guarantee

clauses in IPAM’s BAFO did not get incorporated into the final contract.

Facility

Condition Assessments: In the

original IPAM proposal, IPAM would perform all facility condition assessments

on 50 million sq. ft. of State-owned buildings. Within its BAFO, IPAM decreased its price but also proposed

that facility managers (to be hired for the facility management consolidation

process) and not IPAM would perform the condition assessments on the

last 40 million square feet. However,

on February 4, 2005, the Department

published in the Procurement Bulletin a sole source $2.25 million contract

for IPAM to perform facility condition assessments.

Lease Administration Services: In the original IPAM proposal, IPAM proposed “…while not

specifically requested by the State in the RFP, IPAM will offer to provide

future lease administration services to the State on an ongoing basis once

the new system is operational.” The

BAFO submitted by IPAM contained the exact language as the original proposal

with the inclusion of “for an additional fee” at the end of the sentence

quoted above. When questioned on

whether this “additional fee” was outside the purpose of the best and final

process, Department officials indicated that the additional fee was not

outside the process because the services were not part of the original RFP

anyway. On January 20, 2005, the

Department amended the contract with IPAM to increase the contract amount by

$3.5 million for lease transaction services.

(Finding Code No. 04-5, page 25)

We recommended that the Department allow vendors to only

revise sections of proposals as stated within the purpose for requesting a

best and final offer.

The Department disagreed with the finding and recommendation.

FAILURE

TO PUBLISH THAT CONTRACT WAS AWARDED TO OTHER THAN THE LOWEST PRICED VENDOR

The Department failed to provide notification, in the

Illinois Procurement Bulletin, that contracts were awarded to other than the

lowest priced vendor.

Procurement Code provisions applicable to professional and artistic

contracts provide that "when the contract exceeds the $25,000 threshold

and the lowest bidder is not selected, the chief procurement officer or the

State purchasing officer shall forward together with the contract notice of

who the low bidder was and a written decision as to why another was

selected…[CMS] shall publish…notice of the chief procurement officer’s or

State purchasing officer’s written decision.” (30 ILCS 500/35-30 (f))

The Department's administrative rules similarly require, “If the price

of the best qualified vendor exceeds $25,000, the Procurement Officer, but

not a designee, must state why a vendor other than the low priced vendor was

selected and that determination shall be published in the Bulletin.” (44 Ill. Adm. Code 1.2035 (m)(3))

In 44 percent (4 of 9) of the contracts we reviewed, the

Department awarded the contract to a vendor that was not the lowest priced

proposer and did not publish this in the Procurement Bulletin. (Finding Code No. 04-6, page 28)

We recommended that the Department follow the requirements

set forth in the Illinois Procurement Code and administrative rules and

publish instances where a vendor with the lowest price was not selected for

the award of a contract.

The Department disagreed with the finding.

FAILURE

TO INCLUDE SUBCONTRACTOR INFORMATION IN CONTRACTS

The Department failed to ensure that subcontractor

information required under the Procurement Code was included in contracts

awarded by the Department. In 44

percent (4 of 9) of the contracts we reviewed, the Department failed to have

information on subcontractors utilized by the selected vendor included in the

contract. The Department estimated

the value of these contracts to be approximately $53 million.

For professional and artistic contracts only, the contracts

must state, “whether the services of a subcontractor will be used. The contract shall include the names and

addresses of all subcontractors and the expected amount of money each will receive

under the contract.” If a contractor

adds or changes any subcontractors, CMS must receive the foregoing

information in writing in a prompt manner.

(30 ILCS 500/35-40)

For instance:

§

Asset Management Contract: The IPAM contract does not identify any of

the subcontractors utilized by IPAM.

Four subcontractors were identified in the IPAM proposal it submitted

to the Department. However, the

amount to be paid to these subcontractors was not disclosed. Furthermore, during our review of expenses

reimbursed by the State to IPAM, we found evidence that one of the IPAM

subcontractors was utilizing subcontractors of their own to perform work.

§

IT Rationalization Contract: The BearingPoint and Accenture contracts

do not identify any of the subcontractors to be utilized during the IT

Rationalization project. The

proposals do identify some subcontractors but not the amounts each would

receive under the contract. In the

Accenture proposal, three subcontractors are identified. However, after we inquired about the use

of subcontractors and how much each received in compensation, a Department

official collected information that shows Accenture used six subcontractors

on this project and paid them a total of $2.6 million. In the BearingPoint proposal, two subcontractors

are identified. A Department official

collected information that shows BearingPoint subcontracted with eight firms

on this project and paid them a total of $3.2 million for hourly fees plus

expenses.

§

Telecom Rationalization: The EKI contract did not contain

information on the use of any subcontractors. The proposal submitted by EKI did identify four subcontractors

but with no expected value for compensation.

After we inquired about the use of subcontractors and how much each

received in compensation, a Department official collected information that

showed EKI used four subcontractors on this project – including three

different subcontractors that had never been identified in any document we

examined. In documentation supplied

by the Department in February 2005, one of these three subcontractors that

had not been listed in either the contract or the proposal had received $3.2

million from EKI for subcontracting work.

The same documentation showed that EKI had made $1.3 million – or less

than half of what the subcontractor had received.

§

Software Review: In the contract between BearingPoint and the Department (in the

section that allows subcontracting) BearingPoint does assert that it “is

proposing to use an independent consultant to complete a portion of the required

consulting services.” The

subcontractor is not identified in the contract. Department officials did not provide us with information on a

subcontractor or any amount paid by the primary contractor to a

subcontractor. (Finding Code No.

04-7, page 31)

We recommended that the Department follow the direction of

the Illinois Procurement Code and include information on subcontractors and

the amounts to be paid to the subcontractors under the contracts.

The Department disagreed with the finding.

NOT

TIMELY IN EXECUTING CONTRACTS

The Department was not timely in executing contracts with

vendors for contracts awarded.

Additionally, the Department allowed vendors to initiate work on these

projects without a written contract in place.

In 100 percent (9 of 9) of the contracts we reviewed, the

Department allowed vendors to initiate work on the project without a formal

written agreement in place. These

contracts were estimated by the Department to have a maximum contract value

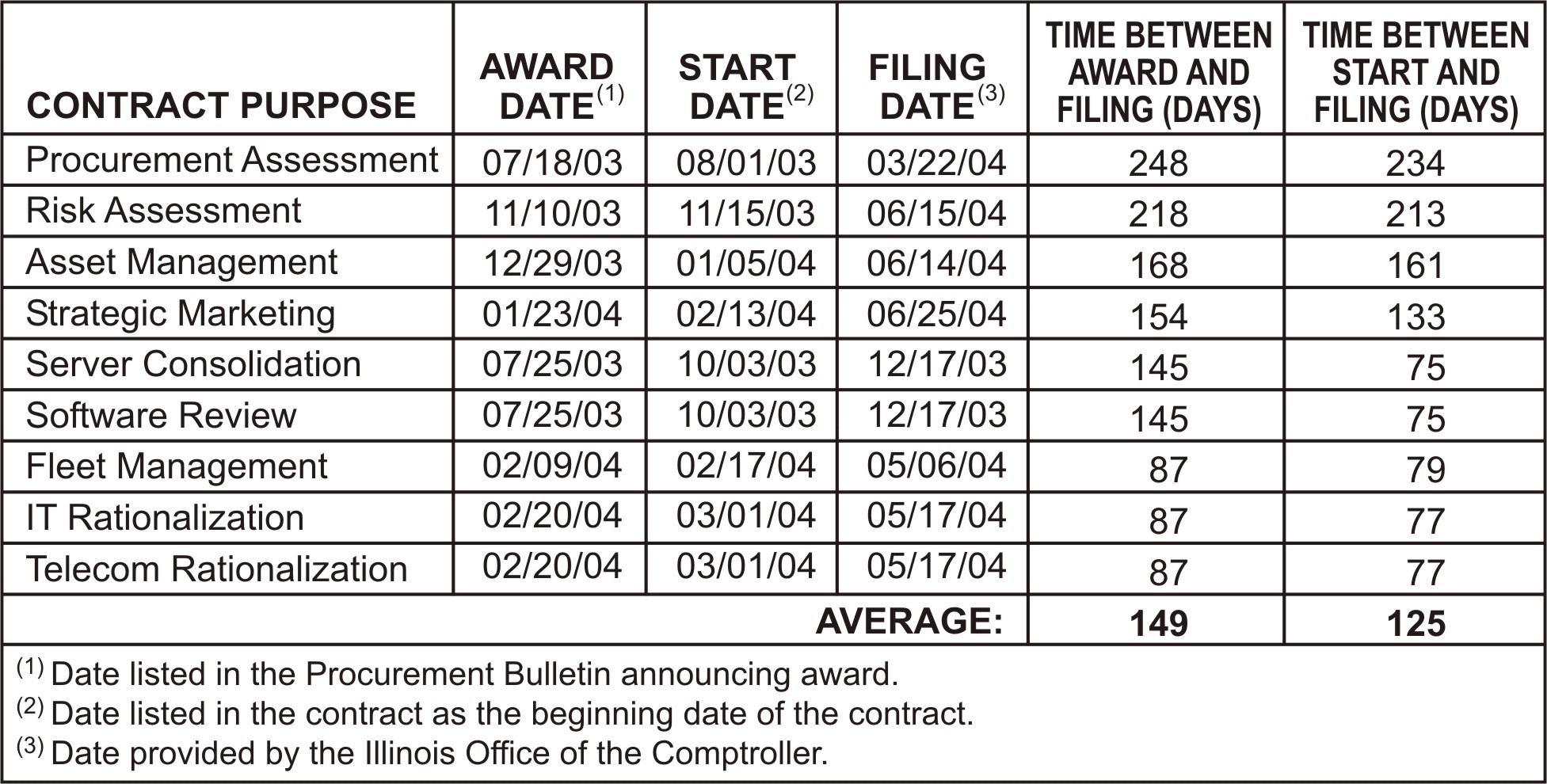

of $69 million with an FY04 financial commitment of $32 million. On average, the length of time between the

announcement of the award and the filing of a contract with the

Comptroller was 149 days (with a range of 87 days to 248 days). The average length of time between beginning

work on the contract and the filing of the contract with the

Comptroller was 125 days (with a range of 75 days to 234 days). The table below provides a breakdown for

all nine contracts reviewed:

|