Chapter One

AUDITOR GENERAL’S SUMMARY

REPORT CONCLUSIONS

On June 18, 2012, Public Act 097-0694 was signed into law which directed the Auditor General to contract with or hire an actuary to serve as the State Actuary. Cheiron was selected as the State Actuary. The Public Act directed the State Actuary to:

· Review assumptions and valuations prepared by actuaries retained by the boards of trustees of the State-funded retirement systems;

· Issue preliminary reports to the boards of trustees of the State-funded retirement systems concerning proposed certifications of required State contributions submitted to the State Actuary by those boards; and

· Identify recommended changes to actuarial assumptions that the boards must consider before finalizing their certifications of the required State contributions.

Cheiron reviewed the actuarial assumptions used in each of the five systems’ actuarial valuations for the year ended June 30, 2013 and concluded that they generally were reasonable. Cheiron did not recommend any changes to the assumptions used in the June 30, 2013 actuarial valuations. Cheiron did, however, raise concerns regarding the interest rate assumptions used by three of the systems (SERS, SURS, and TRS) and recommended for the upcoming June 30, 2014 valuations that the interest rates be lowered. Should the Boards decide not to lower their interest rate assumptions, Cheiron requested that the Boards provide Cheiron with substantial justification as to why the rates should not be lowered.

Cheiron made recommendations for additional disclosures for the 2013 valuations and also recommended changes for future valuations. Recommendations included the following:

· The SERS, SURS, and TRS actuarial valuations should more fully analyze and disclose the source of losses which have been occurring, but not fully explained, in the valuations for several years. While last year’s State Actuary report recommended that these losses be explained, corrective action was not taken.

· The Boards should annually review the interest rate and inflation assumptions as opposed to waiting for the completion of a formal experience study.

· The systems’ actuaries, in future valuations, should consider establishing a corridor that would limit the maximum spread between the actuarial value of assets (smoothed value) and the market value of assets so that the actuarial value of assets, in any year, would be no more than 120 percent of market value or no less than 80 percent of market value. A move to this approach would have no impact on the 2013 actuarial valuation results as the actuarial value of assets for all five systems is currently within the 80 percent to 120 percent corridor.

· The systems should use fully generational mortality tables.

Cheiron verified the arithmetic behind the calculations made by the systems’ actuaries to develop the required State contribution and reviewed the assumptions on which the calculations were based. Cheiron recommended that the systems’ actuaries disclose additional information in future valuation reports.

The Illinois Pension Code requires that the systems’ actuaries calculate the required State contribution using a prescribed funding method that achieves 90 percent funding in the year 2045. Cheiron concluded that this funding method does not meet actuarial standards of practice because the systems are not targeted to be funded at 100 percent and the funding of the plans is pushed back to later years. At a minimum, future plan benefit accruals should be fully funded, to avoid continued systematic underfunding of the systems. Furthermore, based on the systems’ 2013 actuarial valuation reports, the funded ratio of the systems ranged from 41.5 percent (SURS) to 16.2 percent (GARS) based on the actuarial value of assets as a ratio over the actuarial liability. Cheiron has concerns about the solvency of the systems if there is a significant market downturn. Cheiron suggests, due to the systematic underfunding of the systems, that the systems’ Boards always use the conservative end of any range of assumptions recommended by their actuaries. Cheiron also recommended stress testing be done to determine whether there will be sufficient assets to pay benefits if there is a significant market downturn.

Information presented in this report is based on State statute in effect at June 30, 2013 and does not take into consideration any effect of Public Act 98-599, signed by the Governor on December 5, 2013.

INTRODUCTION AND BACKGROUND

On June 18, 2012, Public Act 097-0694 was signed into law which directed the Auditor General to contract with or hire an actuary to serve as the State Actuary. The Public Act amended the Illinois State Auditing Act as well as sections of the Illinois Pension Code for each of the five State-funded retirement systems. The five State-funded retirement systems are:

· The Teachers’ Retirement System (TRS);

· The State Universities Retirement System (SURS);

· The State Employees’ Retirement System (SERS);

· The Judges’ Retirement System (JRS); and

· The General Assembly Retirement System (GARS).

Requirements of Public Act 097-0694

Public Act 097-0694 requires the State Actuary to conduct an annual review of the valuations prepared by the actuaries of the State-funded retirement systems. Specifically the Act requires the State Actuary to:

· Review assumptions and valuations prepared by actuaries retained by the boards of trustees of the State-funded retirement systems;

· Issue preliminary reports to the boards of trustees of the State-funded retirement systems concerning proposed certifications of required State contributions submitted to the State Actuary by those boards; and

· Identify recommended changes to actuarial assumptions that the boards must consider before finalizing their certifications of the required State contributions.

On or before November 1 of each year, beginning November 1, 2012, the boards of each of the systems must submit to the State Actuary a proposed certification of the amount of the required State contribution to the system for the next fiscal year, along with all of the actuarial assumptions, calculations, and data upon which that proposed certification is based.

On or before January 1, 2013, and each January 1 thereafter, the Auditor General shall submit a written report to the General Assembly and Governor documenting the initial assumptions and valuations prepared by actuaries retained by the boards of trustees of the State-funded retirement systems, any changes recommended by the State Actuary in the actuarial assumptions, and the responses of each board to the State Actuary's recommendations.

On or before January 15, 2013, and every January 15 thereafter, each Board shall certify to the Governor and the General Assembly the amount of the required State contribution for the next fiscal year. The Board's certification must note any deviations from the State Actuary's recommended changes, the reason or reasons for not following the State Actuary's recommended changes, and the fiscal impact of not following the State Actuary's recommended changes on the required State contribution.

Contracting with the State Actuary

On July 12, 2012, the Office of the Auditor General issued a Request for Proposals for the services of a State Actuary. On August 24, 2012, the contract was awarded to Cheiron. Cheiron is a full-service actuarial and consulting firm with offices in nine locations throughout the United States. Cheiron has experience working with multiple public pension plans around the country.

REVIEW OF THE ACTUARIAL ASSUMPTIONS

Cheiron reviewed the actuarial assumptions used in each of the five systems’ actuarial valuations for the year ended June 30, 2013 and concluded that they generally were reasonable. Cheiron did not recommend any changes to the assumptions used in the June 30, 2013 actuarial valuations. Cheiron did, however, raise concerns regarding the interest rate assumptions used by three of the systems (SERS, SURS, and TRS) and recommended for the upcoming June 30, 2014 valuations that the interest rates be lowered. Should the Boards decide not to lower their interest rate assumptions, Cheiron requested that the Boards provide Cheiron with substantial justification as to why the rates should not be lowered.

Cheiron also made recommendations for additional disclosures for the 2013 valuations and recommended changes for future valuations. In their responses to Cheiron’s preliminary reports, systems indicated that they were planning to add to their 2013 valuations some of the additional disclosures recommended by Cheiron. The systems’ responses to Cheiron’s preliminary reports can be found in Appendix C of this report.

Exhibit 1-1 summarizes the recommendations made for the various retirement systems. At the end of each of the reports located in Chapters 2 through 6 is a chart summarizing the status of recommendations made by the State Actuary in the 2012 report.

|

Exhibit 1-1 RECOMMENDATIONS TO THE RETIREMENT SYSTEMS |

|||||

|

Recommendations |

TRS |

SURS |

SERS |

JRS |

GARS |

|

Recommended Changes to Actuarial Assumptions used in the 2013 Actuarial Valuations: |

|||||

|

Cheiron did not recommend actuarial assumption changes this year. However, Cheiron recommended that the interest rate assumptions used by SERS, SURS, and TRS be lowered for the upcoming June 30, 2014 valuation. |

|||||

|

Recommended Additional Disclosures for the 2013 Actuarial Valuations: |

|||||

|

· Include normal cost development in all projections |

X |

|

|

|

|

|

· Disclose a detailed breakdown of the actuarial liabilities for each participant class |

X |

|

|

|

|

|

· Include a reconciliation of the implication of the census data lag for the inactive data |

X |

|

|

|

|

|

· Expand discussion of the change in the treatment of federal funds contribution rate |

X |

|

|

|

|

|

· Provide additional analysis and more thorough disclosure to help determine the source of unexplained losses |

X |

X |

X |

|

|

|

· More completely describe the active participant mortality table and the administrative expense rate |

X |

|

|

|

|

|

· Include an explicit development that shows all sub-components and additional details related to the development of the required State contribution |

X |

|

|

|

|

|

· Explain the rationale to lower the Effective Rate of Interest |

|

X |

|

|

|

|

Recommended Changes for Future Actuarial Valuations: |

|||||

|

· Annually review the interest and inflation rate assumptions and adjust assumptions accordingly |

X |

X |

X |

X |

X |

|

· Consider establishing a corridor around the market value of assets of 80% to 120% beyond which the actuarial value is limited |

X |

X |

X |

X |

X |

|

· Disclose additional items useful to review the system’s funded status in 2045 (such as future benefit payouts split by active and inactives, and/or splitting active member information into specified groups) |

X |

|

X |

X |

X |

|

· Include changes made as a result of the State Actuary review in its valuation report (rather than in a supplement) |

X |

|

|

|

|

|

· Other minor recommendations |

X |

X |

X |

X |

X |

|

· Include historic development of assets without Government Obligation Bonds |

X |

X |

X |

X |

X |

|

· Consider using a fully generational mortality table |

|

X |

X |

X |

X |

|

· Disclose the specific data referred to in the description as to how the new entrant profile assumption was developed |

|

X |

X |

X |

X |

|

· Consider increasing the 1% of salary load for disability benefits |

|

|

X |

|

|

|

Source: OAG summary of Cheiron’s preliminary reports to the five State-funded retirement systems. |

|||||

The following sections discuss some of the key assumptions and recommendations. Further details on the assumptions and recommendations, including those not discussed in this summary chapter, are contained in the State Actuary’s preliminary reports for each of the five systems, found in chapters 2 through 6 of this report.

Economic Assumptions

Cheiron reviewed the economic assumptions utilized in the actuarial valuations for each of the five State-funded retirement systems. The following sections discuss two of those assumptions – the interest rate assumption and the inflation assumption.

Interest Rate Assumption

The interest rate assumption (also called the investment return or discount rate) is the most impactful assumption affecting the required State contribution amount. This assumption is used to value liabilities for funding purposes. The retirement systems use varying interest rate assumptions. Exhibit 1-2 shows the interest rate assumptions for each of the five State-funded retirement systems. As can be seen in the exhibit, since 2010, each of the systems lowered its interest rate assumption.

|

Exhibit 1-2 INTEREST RATE ASSUMPTIONS FOR THE FIVE STATE-FUNDED RETIREMENT SYSTEMS |

||

|

System |

Interest Rate |

Notes |

|

Teachers’ Retirement System |

8.00% |

Lowered from 8.50% for the June 30, 2012 actuarial valuation |

|

State Universities Retirement System |

7.75% |

Lowered from 8.50% for the June 30, 2010 actuarial valuation |

|

State Employees’ Retirement System |

7.75% |

Lowered from 8.50% for the June 30, 2010 actuarial valuation |

|

Judges’ Retirement System |

7.00% |

Lowered from 8.00% for the June 30, 2010 actuarial valuation |

|

General Assembly Retirement System |

7.00% |

Lowered from 8.00% for the June 30, 2011 actuarial valuation |

|

Source: Retirement system actuarial reports and experience studies. |

||

Based on the evidence which the systems provided, Cheiron concluded that it was not comfortable with the interest rate assumptions used by three of the systems (TRS, SURS, and SERS). Cheiron noted that in last year’s State Actuary report to the Auditor General and the three systems, Cheiron recommended that the SERS, SURS, and TRS Boards consider lowering the interest rate for the June 30, 2013 valuation. None of the Boards reduced the interest rate assumption. In light of the evidence Cheiron presented in the individual system’s reports, Cheiron urged the Boards to lower the interest rate assumption for the upcoming June 30, 2014 actuarial valuation. If the Boards conclude that a reduction is not needed, Cheiron requested that the Boards provide substantial justification for maintaining the current interest rate.

Below are examples of the evidence cited by Cheiron to support its recommendation to lower interest rate assumptions for the upcoming June 30, 2014 valuations:

· SERS – Cheiron recommended decreasing the interest rate assumption from 7.75 percent to 7.25 percent or lower for the upcoming 2014 valuation: SERS’ actuary reported to the SERS Board in February 2013, that the expected average geometric return on SERS’ investments over the next 30 years, as developed by eight national investment consulting firms, is 7.09%. The SERS actuary also noted that the probability of meeting or exceeding the 7.75% assumption is 38.6%. Cheiron concluded that selecting an assumption that has a 61.4% chance of not being met is unreasonable.

Cheiron also noted that the Judges’ Retirement System (JRS) and the General Assembly Retirement Systems (GARS) have their investments commingled with the SERS investments and managed as one large investment pool. Both JRS and GARS use a 7.0 percent interest rate assumption. It is not clear how a 7.75 percent assumption for SERS can be justified when a 7.0 percent assumption is used for the two other systems.

· SURS – Cheiron recommended decreasing the interest rate assumption from 7.75 percent to 7.25 percent or lower for the upcoming 2014 valuation: A 2013 review of SURS’ capital market assumptions showed an expected geometric return on the System’s portfolio to be 6.95 percent over a 5- to 10-year time horizon. This expected return has declined 55 basis points since an earlier report in 2011. Furthermore, in SURS’ 2010 experience study, the system’s actuary relied on the opinion of nine independent investment consultants who provided that the probability of exceeding 7.75 percent investment return each year was 44.59 percent. Therefore, it can be inferred that for this assumption the expected average return rate based on the current asset allocation is lower than 7.75 percent.

· TRS – Cheiron recommended decreasing the interest rate assumption from the current 8.00 percent. TRS provided Cheiron with a one page analysis from its actuary that indicated an expectation of the average return over the next 30 years at 8.37 percent. However, the communication lacked any supporting documentation of assumptions to arrive at this value. Furthermore, the 8.37 percent expected rate of return contradicted the expectations of TRS’s investment consultant. The TRS investment consultant’s June 30, 2013 Investment Performance Review provided historic TRS returns that for all periods, except the one year and 20 year averages, with rates significantly below 8.0 percent. These lower actual returns are evidence to infer that expectations of a repeat of the 1990’s, which is included in the 20 year average, is not anticipated by investment consultants to be repeated. The 15 year average is 7.7 percent.

Cheiron recommended that the five Boards annually review the interest rate and inflation rate assumptions. Cheiron offered several different rationales for considering lowering the interest rate in future valuations. These included:

· A review of the interest and inflation rates does not involve the collection of significant data, and can easily be updated annually. In addition, it keeps the Boards focused more closely on these very important assumptions.

· The Statutory funding requirement cannot be ignored in the choice of an appropriate interest assumption. Fundamental to the Statute is the requirement to determine the appropriate portion of unfunded liability to be funded each year that produces a level amortization amount as a percent of future projected payroll. If the interest assumption is expected to result in a higher likelihood of returns below the rate than above, then by definition, this will produce lower than expected returns and an increasing amortization amount as a percent of payroll.

· The federal government, which promulgates minimum funding standards for corporate pension plans, already requires corporate pension plans to utilize interest assumptions that are based on short-term and mid-term bond rates, which are very low.

· Pension Industry (actuarial, accounting, legal, and investment professional organizations) pressures may lead to mandated lower interest rates: In recent years, there has been increased and controversial movement in the actuarial community that actuaries must move away from the traditional theory where the assumed interest assumption is based on expected plan earnings, and instead employ theories espoused by financial economists. Under financial economic theory, the interest rate used to value pension plan liabilities should be based on near risk free rates of return, because pension liabilities (or benefit payments) are considered more akin to bonds, and that using the higher expected earnings rates hides the risks of achieving that return. Near risk free rates of return today would be less than 4 percent and would enormously increase the liabilities of the systems and the resulting required State contribution. While this debate continues and has not been resolved, there are external signs that the public sector may ultimately be forced to utilize much lower investment assumptions.

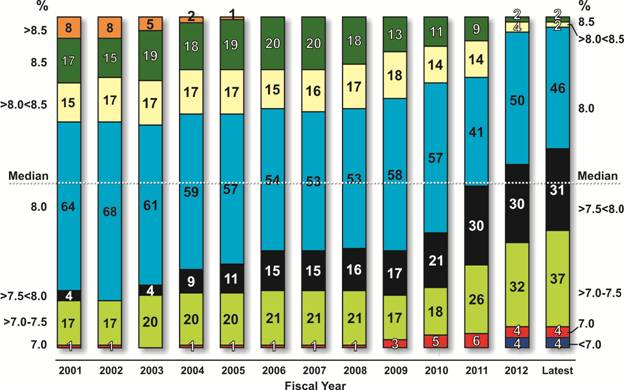

Cheiron also discussed the nationwide movement among pension plans to lower the interest rate assumption. The National Association of State Retirement Administrators (NASRA) conducts the Public Fund Survey which is an online compendium of key characteristics covering 126 public pension plans. Exhibit 1-3 shows the change in the interest rate assumptions, since the inception of the Public Fund Survey in 2001, for 126 public pension plans.

Exhibit 1-3

CHANGE IN INTEREST RATE ASSUMPTIONS SINCE 2001

126 PENSION PLANS IN THE NATION’S LARGEST PUBLIC RETIREMENT SYSTEMS

Source: NASRA Public Fund Survey.

The exhibit shows the shift to lower interest rate assumptions. In 2001, 104 of the 126 plans (83%) used an interest rate assumption of 8.0 percent or higher. The most recent data shows that this number has dropped to only 50 of 126 plans (40%) that use an interest rate of 8.0 percent or higher. The median assumption has fallen below 8.0 percent. Also, four plans have adopted a rate below 7.0 percent.

Inflation Assumption

The inflation assumption primarily impacts the salary increase assumption. The five State-funded retirement systems use inflation assumptions ranging from 2.75 percent to 3.25 percent. Exhibit 1-4 shows the inflation assumptions for each of the five systems.

|

Exhibit 1-4 INFLATION ASSUMPTIONS FOR THE FIVE STATE-FUNDED RETIREMENT SYSTEMS June 30, 2013 Valuation |

||

|

System |

Inflation Rate |

Notes |

|

Teachers’ Retirement System |

3.25% |

Lowered from 3.50% for the June 30, 2012 actuarial valuation |

|

State Universities Retirement System |

2.75% |

Lowered from 3.75% for the June 30, 2011 actuarial valuation |

|

State Employees’ Retirement System |

3.00% |

Lowered from 3.50% for the June 30, 2002 actuarial valuation |

|

Judges’ Retirement System |

3.00% |

Lowered from 4.00% for the June 30, 2011 actuarial valuation |

|

General Assembly Retirement System |

3.00% |

Lowered from 4.00% for the June 30, 2011 actuarial valuation |

|

Source: Retirement system actuarial reports and experience studies. |

||

Cheiron concluded that the inflation assumptions used by the five State-funded retirement systems were within a reasonable range. Cheiron’s rationale for concurring with the inflation assumptions included:

· The 2013 Old-Age, Survivors, and Disability Insurance Trustees Report projects that over the long-term (next 75 years) inflation will average somewhere between 1.8% and 3.8%.

· Cheiron’s comparison of other public sector retirement systems’ inflation assumptions as shown by surveys published by the National Conference on Public Employee Retirement Systems (NCPERS) and Boston College's Center of Public Research (CPR) show that most public sector pension plans utilize an inflation assumption in the range of 2.75 percent to 3.75 percent.

Demographic Assumptions

The retirement systems utilize a number of demographic assumptions such as mortality rates, disability rates, and termination rates. Cheiron reviewed the demographic assumptions and concluded that they were reasonable. Cheiron did, however, make a number of recommendations for additional disclosures for the 2013 valuations and also recommended changes for future valuations concerning various demographic assumptions. For example, Cheiron recommended that systems use a fully generational mortality table.

Also, for several years, the SERS, SURS, and TRS actuarial valuations have reported, but not fully explained, significant losses. Last year, Cheiron recommended that the three systems fully analyze and disclose the source of losses which have been occurring. However, corrective action was not taken by the three systems. This year, Cheiron again recommended that the losses be fully analyzed and, if possible, prefunded through an appropriate assumption.

· SERS: For several consecutive years, there have been significant losses due to retirees from active status which the SERS actuary has explained as being an “extraordinary event which would be difficult to predict in the future.” In the 2013 valuation, the experience loss was $146 million (in 2012 it was $395 million). Given that this event has happened for at least six consecutive years, Cheiron believes that additional analysis and more thorough disclosure is required to help determine the source of these losses.

· SURS: For the past several years, there have been recurring losses for benefit recipients. In the 2013 valuation, the loss was $31.2 million. Cheiron believes that additional analysis and more thorough disclosure is required to help determine the source of these losses.

· TRS: For several consecutive years, there have been significant losses identified in the item Loss due to all other causes in the gain loss section of the actuarial valuation report. In the 2013 valuation, the loss was $254 million. Cheiron believes that additional analysis and more thorough disclosure is required to help determine the source of these losses. The source should be quantified and addressed within the assumptions.

As shown previously, Exhibit 1-1 summarizes the recommendations made for the various retirement systems. Additional details on the demographic assumptions examined can be found in the chapters for each of the five State-funded retirement systems.

PROPOSED CERTIFICATION OF REQUIRED STATE CONTRIBUTION

As required by Public Act 097-0694, each of the five State-funded retirement systems submitted to the State Actuary a proposed certification of the amount of the required State contribution for that system. Cheiron verified the arithmetic behind the calculations made by the systems’ actuaries to develop the required State contribution and reviewed the assumptions on which the calculations were based. Exhibit 1-5 shows the amounts of proposed State contributions submitted by the systems for Fiscal Year 2015.

|

Exhibit 1-5 AMOUNTS OF STATUTORILY REQUIRED STATE CONTRIBUTIONS |

|

|

System |

State Contribution (for Fiscal Year 2015) |

|

Teachers’ Retirement System |

$ 3,412,878,000 |

|

State Universities Retirement System |

1,544,200,000 |

|

State Employees’ Retirement System |

1,748,430,000 |

|

Judges’ Retirement System |

133,982,000 |

|

General Assembly Retirement System |

15,809,000 |

|

Total |

$6,855,299,000 |

|

Source: 2013 retirement system actuarial valuation reports. |

|

Cheiron did, however, recommend that the systems’ actuaries disclose additional information in future valuation reports. To calculate the required State contribution, the systems’ actuaries must make an assumption regarding the new hires that replace existing members over the projection period. This assumption is commonly referred to as the new entrant profile. The new entrant profile is a critical assumption as the required projection of 90 percent funding in 2045 means that the majority of active members at that time will be new hires after the current June 30, 2013 valuation.

Cheiron recommended that the systems’ actuaries disclose additional information as to how the new entrant profile was developed and include all relevant information in their valuation reports to better comply with Actuarial Standard of Practice No. 41 Actuarial Communications.

ACTUARIAL METHODS

Actuarial methods consist of three components: (1) the funding method, which is the attribution of total costs to past, current, and future years; (2) the method of calculating the actuarial value of assets (i.e., asset smoothing); and (3) the amortization basis of the Unfunded Actuarial Liability (UAL). The amortization basis is discussed under the State Mandated Funding Method in the next section.

Information presented in this report is based on State statute in effect at June 30, 2013 and does not take into consideration any effect of Public Act 98-599, signed by the Governor on December 5, 2013.

Funding Method

All of the five State-funded retirement systems use the Projected Unit Credit (PUC) cost method to assign costs to years of service. This method is required under the Illinois Pension Code. Cheiron had no objection to using the PUC cost method as it is an acceptable method that is used by other public sector pension funds. However, Cheiron would prefer the Entry Age Normal (EAN) funding method as it is more consistent with the Pension Code’s requirement for level percent of pay funding.

Under the PUC method, the benefits of active participants are calculated based on their compensation projected with assumed annual increases to ages at which they are assumed to leave the active workforce by any of these causes: retirement, disability, turnover, or death. Only past service (through the valuation date but not beyond) is taken into account in calculating these benefits. The cost of providing benefits based on past service and future compensation is the actuarial accrued liability for a given active participant. Under the PUC cost method, the value of an active participant’s benefits tends to increase more sharply over their later years of service than over their earlier ones.

As a result of this pattern of benefit values increasing, while the PUC method is not an unreasonable method, more plans use the EAN funding method to mitigate this affect. The NASRA Public Fund Survey indicates that only 15 of the 126 public pension plans (12%) use the PUC cost method. It should also be noted that the EAN method will be the required method to calculate liability for the new Governmental Accounting Standards Board Statements 67 and 68.

Asset Smoothing Method

The actuarial value of assets for the systems is a smoothed market value. Unanticipated changes in market value are recognized over five years in the actuarial value of assets. The primary purpose for smoothing out gains and losses over multiple years is that the fluctuations in the actuarial value of assets will be less volatile over time than fluctuations in the market value of assets. Cheiron concurred with the use of the asset smoothing method noting that smoothing the market gains and losses over a period of five years to determine the actuarial value of assets is a generally accepted approach in determining actuarial cost.

Another aspect of asset smoothing methods is whether or not to limit the maximum spread between the actuarial value of assets (smoothed value) and the market value of assets. Many public sector pension plans limit the actuarial value of assets to, in any year, no more than 120 percent of market value or no less than 80 percent of market value. In fact, the Internal Revenue Service (IRS) mandates this "corridor" for private sector pension plans (a 90%-110% corridor is mandated). Even though it is not mandated for public plans, Cheiron believes that the use of this type of corridor is a much sounder actuarial practice. According to Actuarial Standard of Practice No. 44 Selection and Use of Asset Valuation Methods for Pension Valuations 3.3(b)(1), the actuarial value of assets should ". . . fall within a reasonable range around the corresponding market values." Therefore, Cheiron recommended that the Boards consider moving to this approach in future valuations. Cheiron also noted that a move to this approach would have no impact on the 2013 actuarial valuation results as the actuarial value of assets for all five systems is currently within the 80 percent to 120 percent corridor. The systems have indicated that the current method is prescribed in statute and that a change would require legislative action.

OTHER ISSUES

Cheiron raised three other issues in its reports to the retirement systems. The first issue related to the State mandated funding method, the second issue related to the State mandated projection method, and the third was a status review of the systems’ preparation for the implementation of the new GASB Standards Nos. 67 and 68.

State Mandated Funding Method

The Illinois Pension Code requires that the systems’ actuaries base the required contribution using a prescribed funding method that achieves 90 percent funding in the year 2045. In the actuarial valuation reports, the systems’ actuaries discuss their concerns issues with this funding method.

· In SURS’ June 30, 2013 actuarial valuation report, SURS’ actuary comments that the current funding policy defers funding which puts the system at risk that benefit obligations will not be met. They recommend a funding policy based on 100 percent funding within thirty years.

· In the actuarial valuations for SERS, GARS, and JRS, the actuary advises “strengthening the current statutory funding policy” and provides the following examples:

a. Reducing the projection period needed to reach 90 percent funding;

b. Increasing the 90 percent funding target;

c. Separating the financing of benefits for members hired before and after December 31, 2010; and

d. Changing to an Annual Required Contribution based funding approach with an appropriate amortization policy for each respective tiered benefit structure.

· In its transmittal letter with TRS’ June 30, 2013 actuarial valuation report, TRS’ actuary clearly states their criticism over the fact that the required State contribution to TRS is limited by the Illinois Pension Code (40 ILCS 5/16-158) which, in their opinion, results in a deficient contribution from an actuarial point of view. The Pension Code requires that the actuary base the required contribution using a prescribed funding method that achieves a 90 percent funding in the year 2045. TRS’ actuary’s opinion is that the minimum contribution level should be 100 percent funding within thirty years.

Cheiron concluded that this funding method does not meet actuarial standards of practice because the systems are not targeted to be funded at 100 percent and the funding of the plans is pushed back to later years. At a minimum, future plan benefit accruals should be fully funded, to avoid continued systematic underfunding of the systems. Furthermore, based on the systems’ 2013 actuarial valuation reports, the funded ratio of the systems ranged from 41.5 percent (SURS) to 16.2 percent (GARS) based on the actuarial value of assets as a ratio over the actuarial liability. Cheiron has concerns about the solvency of the systems if there is a significant market downturn. Cheiron suggests, due to the systematic underfunding of the systems, that the systems’ Boards always use the conservative end of any range of assumptions recommended by their actuaries. Cheiron also recommended stress testing be done to determine whether there will be sufficient assets to pay benefits if there is a significant market downturn.

State Mandated Projection Method

Cheiron noted that under the Pension Code, the actuarial methodologies utilized in performing the 2045 projection of the systems’ funded status assume that the future earnings rate is applied to the actuarial value of assets (smoothed value) rather than the market value of assets. If the actuarial value of assets (smoothed value) is higher than the market value of assets, the assets of the system would have to earn a much higher rate of return than what was projected. Cheiron recommended that consideration be given to requiring that the projected future earnings of the systems be based on the starting market value of assets rather than the smoothed value of assets.

Preparation for GASB 67 and 68

The Governmental Accounting Standards Board (GASB) adopted Statement No. 67 (GASB 67) Financial Reporting for Pension Plans—an amendment of GASB Statement No. 25 and Statement No. 68 (GASB 68) Accounting and Financial Reporting for Pensions—an amendment of GASB Statement No. 27. GASB 67 is effective for periods beginning after June 15, 2013 and GASB 68 is effective for fiscal years beginning after June 15, 2014. The following is a brief summary of some of the changes contained in these Statements:

· The total pension liability will be calculated using the individual entry age actuarial cost method.

· A new blended discount rate assumption will be based on (1) a long-term expected rate of return on pension plan investments to the extent that assets are projected to be sufficient to pay benefits based on future contributions intended to finance current member benefits (i.e., excluding normal cost contributions for new entrants) and (2) a tax-exempt, high-quality municipal bond rate to the extent that the conditions for use of the long-term expected rate of return are not met. This will likely mean the discount rate will be reduced if projected contributions plus assets are not able to cover projected pension benefits.

· The unfunded actuarial liability, now called net pension liability, will be calculated using the market value of assets instead of the smoothed actuarial value of assets.

· The entire net pension liability will be recognized immediately on the employer’s statement of net position.

· The annual required contribution (ARC) has been eliminated.

· Recognition periods of unexpected changes in net pension liability would vary depending upon the source for the change. These periods would be immediate for plan changes, five years for the difference between projected and actual investment earnings, and expected working lifetime of both active and inactive members for other total pension liability changes.

Cheiron reviewed each of the systems’ strategy for implementing GASB 67 and 68. For the most part, the systems were in the early planning stages of implementing the new Standards. All five systems had established implementation dates for GASB 67; only SURS specified an implementation date for GASB 68. Some systems had decided what discount rates and allocation methods to use for net pension liability; others were still in the process of exploring these issues. Chapters 2 through 6 of this report contain additional details regarding each of the systems’ implementation plans.

RESPONSES TO THE RECOMMENDATIONS

Each of the five State-funded retirement systems provided responses to Cheiron’s recommendations contained in the preliminary reports. The systems generally agreed with Cheiron’s recommendations. The complete responses are in Appendix C.